How have risks changed in recent years?

Probablity and risk categories.

These are not really new risks

If we are to believe much of the business press, changes to our planet (climate change, globalisation, pollution, drought) have led to the emergence of new risks. This is not entirely true. In fact, traditional finance has long catalogued the full range of economic, environmental and social risks that are likely to emerge. For example, as early as the 7th century BC, Thales is said to have used the risk of crop fluctuations to enrich himself - he rented all the oil presses in advance, anticipating a bumper harvest. So, without being too defensive of finance or economics, we are prepared to bet that there are no new types of risk that have not been identified in the past. There are, of course, a few exceptions: new risks can arise, in particular because of negative feedback loops. But in the list of all the risks affecting economic life, the overwhelming majority correspond to risks that have been identified for several decades or even centuries.

It is mainly the probability of risks that has changed

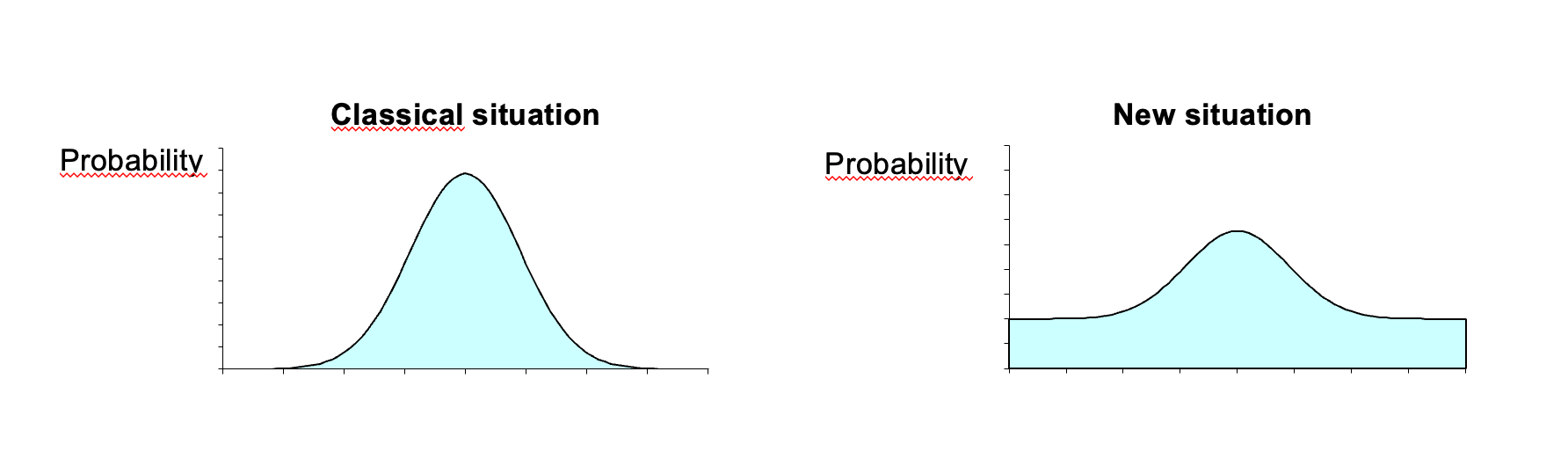

The real question is not to identify a new category of risk, but how it is distributed. Indeed, if we had to sum up the evolution of risks in a single idea, it would be that extreme risks are no longer as extreme as they used to be. The two charts below show the world before (let's say before Greta Thunberg) and the world we live in today.

The figure on the left shows a risk distribution that follows a classical normal distribution. Extreme risks are extremely unlikely, and as the curve moves away from the centre (to the left for negative risks, to the right for positive events) the probabilities become infinitesimal. In statistical jargon, we say that the tails of the distribution are thin. In contrast, the graph on the right shows a probability distribution that also follows a normal distribution, but with thick tails: extreme events are much more likely to occur.

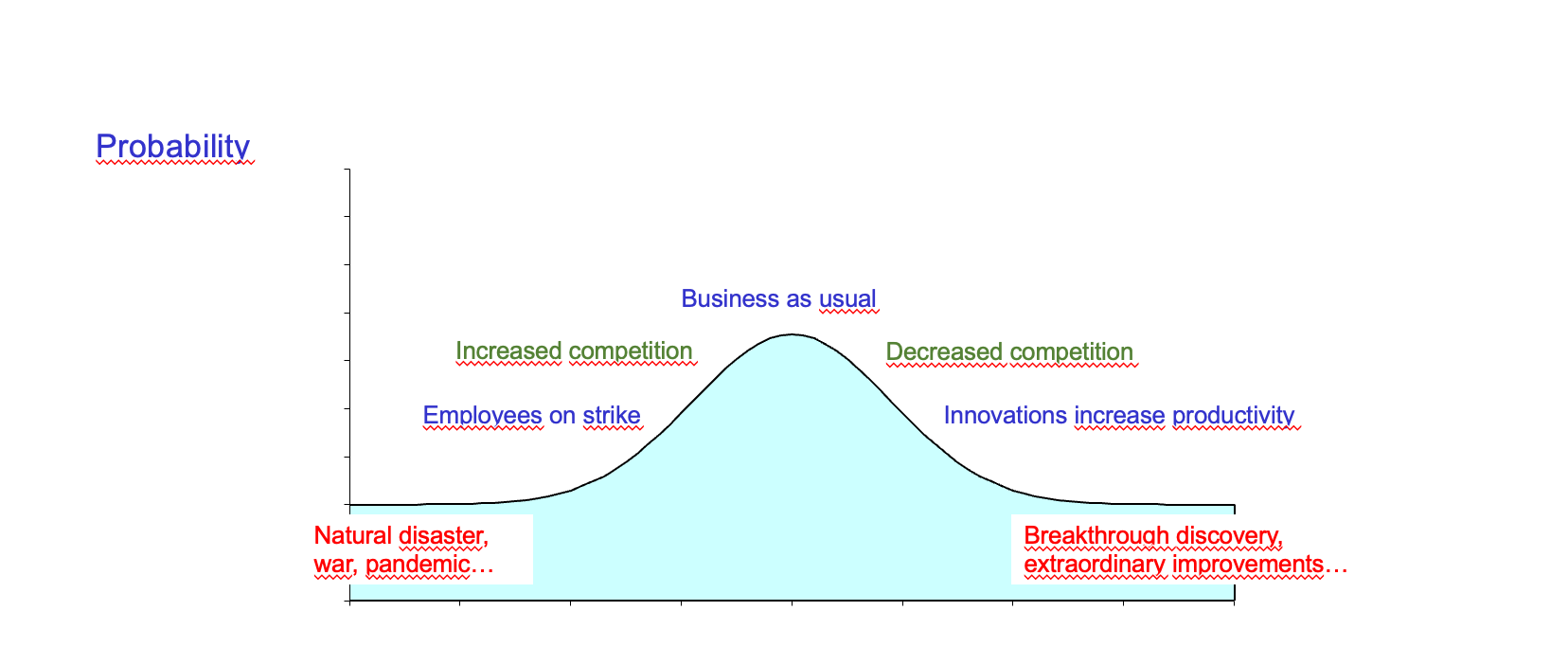

In the figure above, we have reproduced the classic corporate risk figure, but with a change in the probability structure: extreme events are now on our radar as possible eventualities, rather than statistical anomalies that occur only once a century.

Looking back just five years, who could have imagined that a pandemic would reach global proportions, causing 4 billion people to be quarantined for several weeks, while most businesses would have to slow their activities to an unprecedented degree? What was once the stuff of science fiction has become a daily reality for most of the world's population, with consequences that will be felt for years to come. Similarly, who could have predicted a war on European soil, such as Russia's invasion of Ukraine in February 2022? Once again, an extreme event is having consequences that will be felt for years to come (migration, infrastructure, changes in energy policy, geopolitical polarisation, etc.).

Today's risks are not the same as yesterday's

Another change is apparent in the nature of the most likely risks. For older people – including the author – the end of the 20th century and the beginning of the 21st century were marked by the pre-eminence of economic and financial risks: the Internet bubble of 1998 to 2000 and its subsequent stock market crash, the subprime crisis in 2007 followed by the financial crisis of 2008, all against a backdrop of economic globalisation.

These risks were primarily financial, as they stemmed from several decades of financialisation of the economy. Examples include the dematerialisation of paper securities and the concomitant rise of electronic transactions; disintermediation enabled by the development of financial markets, whereby a company can, for example, borrow directly on the bond market; the development of derivative financial products, leading in particular to securitisation, i.e. the transformation of certain physical assets (real estate investments, customer receivables) into equivalent financial products; and, more recently, the cryptocurrency market.

With the development of stock markets on all continents, transactions have taken on an international dimension – with some companies listed on several stock exchanges – and the corresponding risks: a stock market crisis, once confined to a single market, will now spread to other trading platforms as quickly as a forest fire.

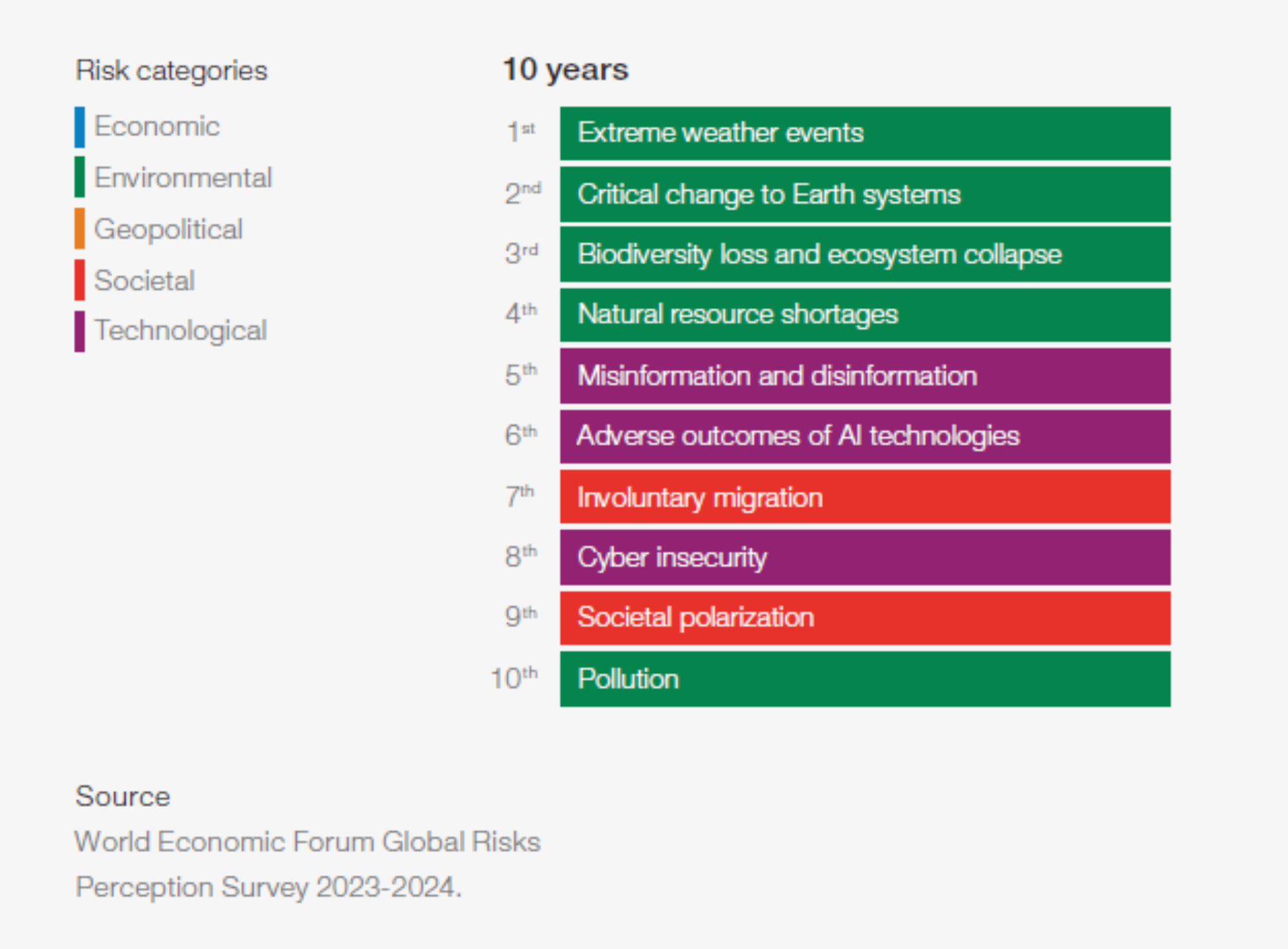

Today, if we refer to the major risks identified by the World Economic Forum[1] for 2024, two striking things can be seen in the following figures.

The first figure lists global risks ranked by severity by 2026. There are two technological risks, two environmental risks, three societal risks and finally two economic risks, ranked 7th and 9th respectively.

The second figure asks the same question, but this time with a 10-year horizon.

In this new figure, we can see that half of the risks are now environmental (four of them are listed first), followed by technological and societal risks. It is also worth noting that, looking ahead to 2034, none of the ten most severe risks are economic.

In summary, no new risks have appeared out of nowhere[2]. Rather, it is the configuration of existing risks that has changed: some extreme risks are now more likely. For example, just a few years ago, who would have ranked biodiversity collapse as the third global risk in terms of impact?

Furthermore, the themes of risk have evolved beyond economic risks. Risks are now mainly related to the environment or social impact, with economic costs that are all the more worrying as these risks have never really been quantified. Indeed, many of these factors, considered as externalities, are not taken into account by companies.

[1] Also known as the Davos Forum.

[2] Even artificial intelligence (AI) is not that new, particularly in finance. Its ancestors are the automation of stock market orders by computers, with all the negative aspects that this entails, such as flash crashes and high-frequency trading.